How to “green” 216 million barrels of Russian crude

Russia's state-owned shipping company, Sovcomflot, received hundreds of millions of dollars in green financing to fund the purchase of LNG-powered oil tankers.

The green financing gap is huge. McKinsey estimates that we need roughly $9.2 trillion of annual investment in infrastructure to reach net zero by 2050. At current levels, we’re $3.5 trillion short on low-carbon spending each year.

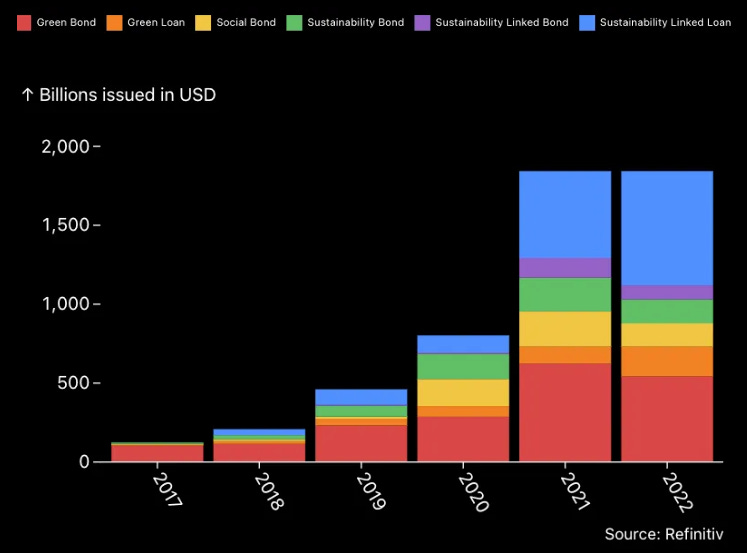

To close this gulf, companies and governments are issuing vast amounts of green and sustainable debt. Despite some mild declines in green bond issuance in recent months, the ethical debt market remains hot with sustainability-linked loans reaching new highs in 2022. At the start of this year, Bloomberg reported that green debt issuance had overtaken debt sales for fossil fuel projects for the first time.

Cash raised through green loans and bonds is meant to go on projects with an environmental benefit. Sustainability-linked bonds and loans are based on a company’s overall performance, rewarding those that hit their ESG targets and, in some cases, penalising firms that don’t by “ratcheting” the interest rate up and down.

With the growth in sustainable and green lending, green projects can more easily get funding and companies are incentivised to hit their sustainability targets. There’s an ever-expanding pool of lenders ready to snap up green bonds and other sustainable debt instruments, at times, making them cheaper than traditional forms of borrowing. On the other side of the equation, financiers can use their green lending to hit their ESG targets.

So far so good.

Another grey-green story

But standardising what counts as green is proving difficult, and in the confusion companies and projects that are more grey than green are able to raise money in sustainable debt markets even when they might be actively harming the environment.

Last week, we found two more examples to add to the growing list of controversial grey-green finance deals.

Sovcomflot — the Kremlin’s very own oil and gas tanker company, now sanctioned by the UK, EU, Canada and the US — received at least two batches of ethical finance that banks may have used to hit their sustainability targets.

Sovcomflot might seem an odd recipient of this type of finance.

First, its primary business is the transportation of fossil fuels, the main driver of anthropogenic warming. Its fleet of 133 tankers shuttles vast payloads of Russian oil and liquefied natural gas (LNG) to Asia and, until recently, Europe. Second, the finance itself was reportedly for building more fossil-fuel-powered tankers to ship more oil.

Sovcomflot isn’t the only company with dubious green financing deals under its belt. Green bonds have been used to fund airport expansions, and sustainability-linked instruments have been used to raise cash for cement companies, oil pipelines and one of the world’s largest and most controversial meat companies linked to vast amounts of tropical deforestation. Such stories have stoked hesitancy amongst investors about ethical debt, leading to some mild cooling of the issuance of green bonds outside of Asia in 2022.

“Borderline greenwashing”

In 2018, Sovcomflot obtained a $252 million sustainability-linked loan from a syndicate of banks — ABN AMRO Bank, BNP Paribas, Citibank, ING Bank, KfW IPEX-Bank and Société Générale — for the purchase of six new Aframax oil tankers to be powered by LNG. The deal was lauded by the industry as a great example of green finance at work with one group awarding it the Green Ship Finance Deal of the Year in 2019.

LNG burns cleaner than traditional tanker fuel releasing about 25% less CO2, and it is touted by Sovcomflot and other shipping groups as the key to decarbonisation. LNG’s transitionary role in fuelling ships, however, is not accepted by everyone in the marine transportation sector. The head of decarbonisation at Maersk, the world’s largest shipping company, has labelled such talk as “borderline greenwashing”. There are also concerns that LNG-powered ships may be leaking significant amounts of methane, a far more potent greenhouse gas than CO2.

Even Sovcomflot doesn’t seem entirely comfortable with the green label for an oil tanker powered by LNG and puts the word “green” in scare quotes on its own website when used to describe the new fleet of Aframaxes that the 2018 loan helped to buy.

216 million barrels of black gold

Wherever you stand on LNG as a shipping fuel, when it comes to Sovcomflot’s green financing for its tankers, it’s worth considering what they’re carrying, not just how they’re powered.

According to data from Refinitiv, since receiving the loan, Sovcomflot’s fleet of six LNG-powered Aframaxes has carried about 216 million tonnes of crude oil to Europe, the US and Asia chartered by some of the world’s biggest fossil fuel companies including Shell, BP, Total and Chevron.

This wasn’t the last time that Sovcomflot managed to secure green financing for building oil tankers. In 2021, it secured a $100 million green loan to build two ice-class shuttle tankers for the Sakhalin-1 project, formerly run by Exxon before its withdrawal from Russia in October last year. The ten-year revolving credit facility was provided by ING Bank, SMBC Bank EU AG and UniCredit Bank.

All this is not to say that marine transportation should not be decarbonised at speed — the world’s current fleet of ships that carry our stuff is phenomenally polluting. The sector emits 940 million tonnes of CO2 per year accounting for around 2.5% of the world’s CO2 emissions and the body responsible for overseeing it has repeatedly failed to agree on a Paris–aligned emission reduction plan.

But does it really make sense for oil tankers powered by LNG — itself a fossil fuel — to be built with green money?

Financing them doesn’t seem a million miles away from funding a pipeline given the critical role shipping plays in moving the world’s oil. Surely, if we’re to close the green financing gap in any meaningful way, it means we have to be spending on the decarbonised energy system of the future. Renewable infrastructure, building efficiency and battery storage come to mind as good investments, not fossil fuel maritime infrastructure.

Defining dark green

In a bid to standardise what is meant by a green investment, the EU is developing its taxonomy for sustainable activities. The first pieces of legislation have not been without controversy. Last year, Client Earth and three other environmental groups began legal action to get the European Commission to drop the “sustainable” label given to natural gas-related activities in the taxonomy’s latest iteration.

For most of the world though, including Asia which is seeing the biggest growth in the issuance of green debt, what is meant by a green loan or bond is murky at best, and where standards exist, they are entirely voluntary. The Climate Bonds Initiative is leading the charge on this, but still, 23% of green bonds issued in 2022 were self-labelled suggesting companies are being left to themselves to decide what colour their debt is.

We’ll be keeping an eye on oddball bits of green finance in the coming months and sharing our notes here.