Decarbonising in the dark

How can we "green" pension portfolios when so much is invested in opaque private equity funds?

Only a third of pension holders have any idea what their money is invested in. Getting a clear picture of what a pension holds isn’t always straightforward, and recent investment trends make it even harder to get an accurate view. This opacity poses a problem for climate campaigners that are pushing pension funds to decarbonise.

Making your money matter

In recent years, campaigns such as Make My Money Matter (MMMM) have encouraged savers to lobby the firms that manage their cash to decarbonise. This is a potentially powerful lever for accelerating the transition with pension funds in the UK, for instance, managing about £3 trillion of assets. According to MMMM, “greening” your pension is 21 times more powerful at cutting your carbon footprint than going vegetarian or giving up flying.

“Greening” a pension portfolio doesn’t necessarily mean divestment. It could mean encouraging your pension to invest in solar and wind projects. It may also mean using share votes to support accelerated transition plans for the polluting companies a pension invests in. Earlier this year, two of the UK’s largest pension funds that manage £130 billion of assets attempted to pressure Shell and BP to cut emissions more aggressively by threatening to vote against the reappointment of company top brass.

The move was not enough to stop Shell from announcing in June that it planned to keep producing oil and gas at current levels, backsliding on its previous commitment to reduce production. This was the last straw for the Church of England Pensions Board — which after years of attempts to engage the oil major — decided to offload its stake.

Divesting fossil fuel companies is meant to make it more costly for them to issue debt in the future, hampering their efforts to expand oil and gas and giving renewables a greater edge. So far, however, this doesn’t seem to be happening. Analysis by Gautam Jain from the Columbia Center for Global Energy Policy suggests that there has been no significant rise in the yield of investment-grade debt issued by oil and gas companies in the years since ESG investing really took off. It seems that more pressure is needed on fossil fuel companies if ESG investing and divestment are going to register on their cost of capital.

Opaque pension investments

One impediment to the strategy endorsed by MMMM is that it is often unclear what fossil fuel assets a pension fund holds, making it harder to actually “green” a portfolio.

On the one hand, it is relatively easy to measure the exposure of a pension pot to publicly listed companies, given that these are often listed in the fund’s disclosures and are straightforward to identify. You can find how much it might own in BP, Exxon or some other major oil and gas company. MMMM have done the sums, and they estimate that UK pension funds hold about £88 billion in public fossil fuel equities.

However, there is another way that pension fund capital is deployed in fossil fuel companies: investments in private equity and infrastructure funds. While infrastructure funds are attractive to pensions for their potential to give stable and long-term returns, they are also a point at which pensions often come into contact with our current fossil-fuel-dominated energy system.

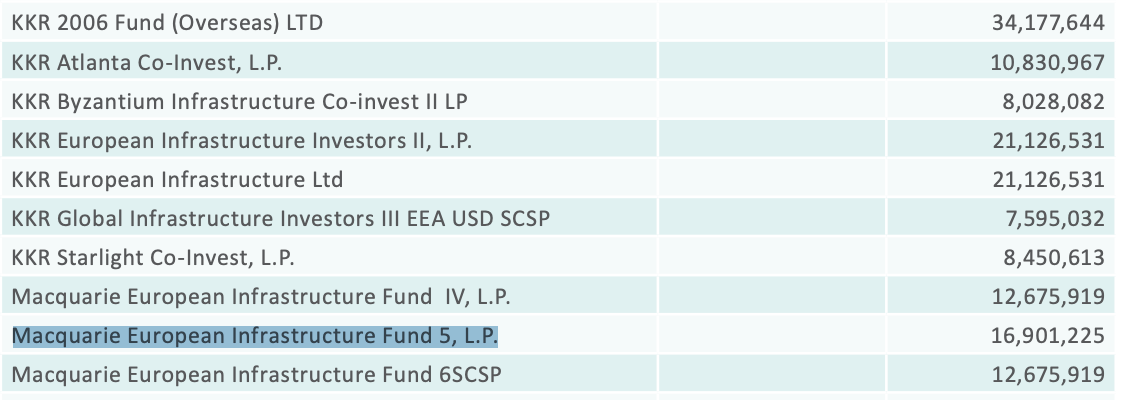

We looked at data from Pitchbook to see where pension funds hold stakes indirectly in some of the most polluting companies through private equity funds. One of our findings was that seven UK public pensions had a stake in a Macquarie infrastructure fund that owned 31% of EP Infrastructure, which in turn owned several coal cogeneration plants and a gas pipeline for transporting Russian gas to Western Europe.

EP Infrastructure is part of the broader EPH group, one of Europe’s biggest polluters. Under the leadership of its CEO, Daniel Křetínský, EPH has made a name for itself by picking up especially dirty bargain basement fossil fuel assets that publicly-listed companies, under pressure from increasingly environmentally-minded shareholders, no longer want on their books.

This has left it with one of Europe's biggest fossil fuel portfolios. According to the climate think tank Ember, EPH is the largest emitter of CO2 from lignite — the most health-harming and climate-damaging form of coal. EPH owns three of the top ten most polluting coal power plants in Europe — all of which run on lignite. Bloomberg profiled Křetínský recently and took a forensic look at what they labelled his bet against the European transition.

The Ferret and The National reported our findings, and you read their coverage here and here.

Left in the dark with no influence

Edinburgh City Council’s pension fund (run by the Lothian Pension Fund) was one of the seven that held an indirect stake in EP Infrastructure via Macquarie. Lothian has been under pressure from campaigners to drop its investment in fossil fuels, and at the end of last year, Edinburgh City Council voted to end its support for oil and gas.

But hidden investments like those in EP Infrastructure are likely to make this process difficult. First, investments like this are hard to identify. In the case of the EP Infrastructure stake, the only thing that appears on the list of holdings is the rather uninformative name of the Macquarie fund (Macquarie European Infrastructure Fund V).

There is the additional problem that where pension funds have chosen to invest in a private equity fund, they have no influence over the final investee. With private equity investment, the pension fund won’t have any corresponding voting shares or board representation that they can use to encourage a company to change.

If climate-conscious pension holders are really going to put pressure on fossil fuel companies, a good measure of transparency around private equity and infrastructure investment is needed.